Understanding foreclosure in Florida is critical to navigating your own home foreclosure.

Foreclosure is no fun. It’s stressful, frustrating, and a negative experience. It results in detrimental credit consequences, preventing you from borrowing money going forward. Your credit can be impacted for as long as 7 to 10 years, ruling out lending for a new house or college. If the bank’s foreclosure action is successful, it will look to evict you as soon as it can. You may have no place to go.

However, foreclosure is not the end of the world. You are not the only person going through this. There are currently 38,145 foreclosure home sales in Florida. In August 2016, 1 in every 808 housing units had received a foreclosure filing.

Focus on understanding how foreclosure works. Armed with that knowledge, you can help reach the best possible solution.

In laymen’s terms, foreclosure is when the banks comes to re-possess your home.

More formally, foreclosure occurs when an owner of property cannot make principal and interest payments on their mortgage. This let’s the lender (usually a bank) seize the property, remove the occupants, and sell the house. The house is sold to pay off unpaid debt.

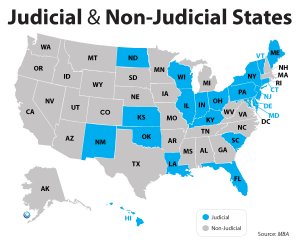

In Florida, judicial foreclosure is the norm. Judicial foreclosure occurs when the bank files litigation in the county where the property is seated and asks the court to enter a judgment permitting the home to be sold to satisfy the debt.

Missing a single mortgage payment will not result in foreclosure in Florida. Rather, a few delinquent payments will be subject to a minor penalty of around 5% of the overdue amount. However, in accordance with the Consumer Financial Protection Bureau rules, once 120 days of delinquency occurs pass, the bank can institute foreclosure proceedings in Florida.

Here is some more detail on judicial foreclosure:

Florida is a “judicial foreclosure” state. The bank must file court proceeding to foreclose.

Your mortgage lender must file suit in the court system.

You’ll get a letter from the court demanding payment.

Assuming the loan is valid, you’ll have 30 days to bring payment to court to avoid foreclosure (and sometimes that can be extended).

If you don’t pay during the payment period, a judgment will be entered and the lender can request the sale of your property – usually through an auction.

Once the property is sold, the sheriff serves an eviction notice and forces you to immediately vacate the property.

House Heroes takes pride in buying difficult to sell property. One of our specialties is helping homeowners stop foreclosure. We will make a fair cash offer for foreclosure houses. In many cases, the amount can cover the debt and you walk away with cash in your pocket. We also help clients with legal fees associated with hiring an attorney to request an extension of the final judgement.

Give us a call (954) 676-1846 to discuss options. Besides selling to House Heroes, options include load modification (“foreclosure workout”), short sale, deed in lieu of foreclosure, and renting.

Outside of Florida: Under Power of Sale (or Non Judicial Foreclosure):

In many areas outside of Florida, foreclosure goes through “power of sale” or “non-judicial foreclosure.” In this scenario, parties with an interest in the property must be notified (as well as judicial foreclosure). Parties with an interest typically include contractors, other bank lending, city liens.

Here is some info on “under power of sale” foreclosures:

The bank serves you papers demanding payment, and the courts are not required – although the process may be subject to judicial review.

After the waiting period ends, a “deed of trust” is written and control of the property is transferred to a trustee. drawn up and control of your property is transferred to a trustee.

The trustee sells the property on behalf the lender at a public auction on notice.

What Happens After A Foreclosure Auction?

When foreclosure finishes, the loan is paid off with the sale proceeds. In some cases, if the sale of the property at auction doesn’t cover the loan, a deficiency judgmentcan be issued against the borrower.

In Florida deficiency judgments are allowed. According to Nolo,

“In Florida, the lender may obtain a deficiency judgment as part of the foreclosure action if the borrower was personally served with the foreclosure complaint. The lender may also file a separate lawsuit against the borrower for a deficiency, unless the court in the foreclosure action has granted or denied a claim for a deficiency judgment.

The judge determines the amount of the deficiency judgment. The court has flexibility regarding the amount of the deficiency. However, it generally cannot exceed the difference between the judgment amount and the fair market value as of the date of sale.”

Banks can seek a deficiency judgment against you if proceeds from the foreclosure sale do not cover the amount owed.

In Florida, the lender may seek a deficiency judgment within 1 year from the date of foreclosure for residential properties with no more than four dwelling units. The reverse isn’t true, however. If the bank sells the house for more than the amount owed, it keeps the difference. Any gain from a later sale goes directly to the lender.

Undoubtedly, you should avoid a foreclosure at all costs. Call up the bank to put together a solution. You can also reach out to a trustworthy real estate investor like House Heroes LLC to rid yourself a Florida house before a judgment is issued.

Experienced investors help negotiating with banks to lower the amount you owe in a sale, make a short sale offer, connect you with a short sale negotiator and foreclosure attorney.

Be wary of foreclosure scams. Offers and advice that are “too good to be true” probably are. Companies often try to charge a fee for “counseling services”, or may ask you to sign over title to your property, re-direct mortgage payments. An unethical company might ask to you make payments to them directly to pay the mortgage – but then keep the payments for themselves. Here are some tips from Fannie Mae to identify potential scams.

If you need to sell a property in Florida, we are here to help.

{kind=link}